Some of you may thinks Monte Carlo is a name of a place, or some mountain located at some countries. But in mathematics Monte Carlo is a way to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables (https://www.investopedia.com/terms/m/montecarlosimulation.asp).

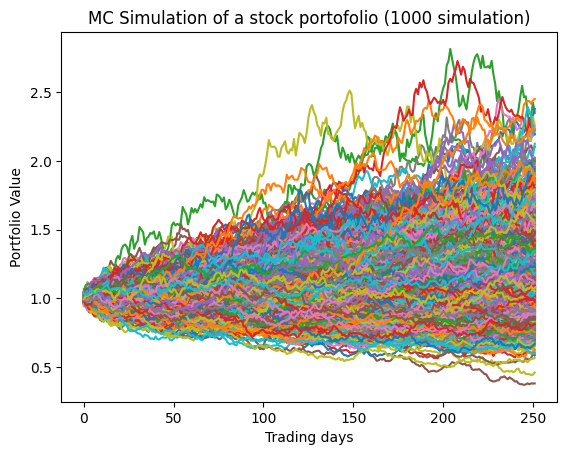

In order to use Monte Carlo simulation to optimize the portfolio first we need to collect the stocks data and do calculation for annualized mean return, standard deviation, variance in order to get volatility. By all that variable we can model the stocks return movement using Geometric Brownian Motion and combine it with monte carlo simulation so we get the probabilities for both the return and the reward.

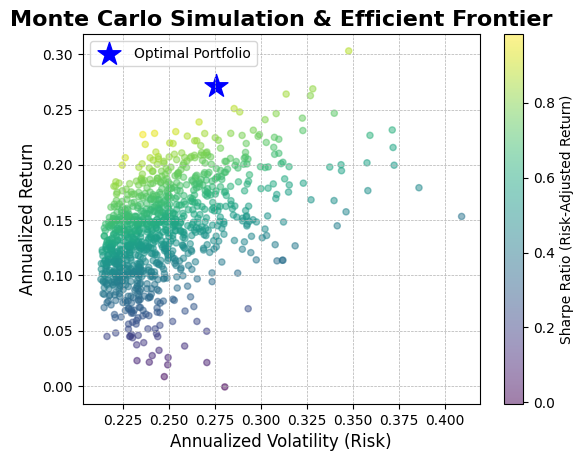

After that, we use monte carlo simulation to randomized a thousand of probabilities of the equities allocation and using efficient frontier to get the optimized point where the we get maximized return with minimal volatility (highest sharpe). by that we get the portfolio allocation that optimized by monte carlo simulation.

this is the project github if you want try it! https://github.com/RinoWana/Portfolio-Optimization-using-Monte-Carlo-Simulation